The DealMakers AFRICA Q1 2026 is out now!

DealMakers AFRICA Annual Awards - March 2026

Lagos, Nigeria & Nairobi, Kenya: View pictures

DealMakers AFRICA Q1 2026 issue

M&A Regional Analysis | PE Regional Analysis | Largest M&A Deals Q1 2026

East Africa Awards 2025 | Nairobi, Kenya | March 2026

West Africa Awards 2025 | Lagos, Nigeria | March 2026

THORTS

by Daniel Outré | Enexus

by Konrad Fleischhauer and Kayla Jackson | PSG Capital

CONTENTS

FROM THE EDITOR'S DESK

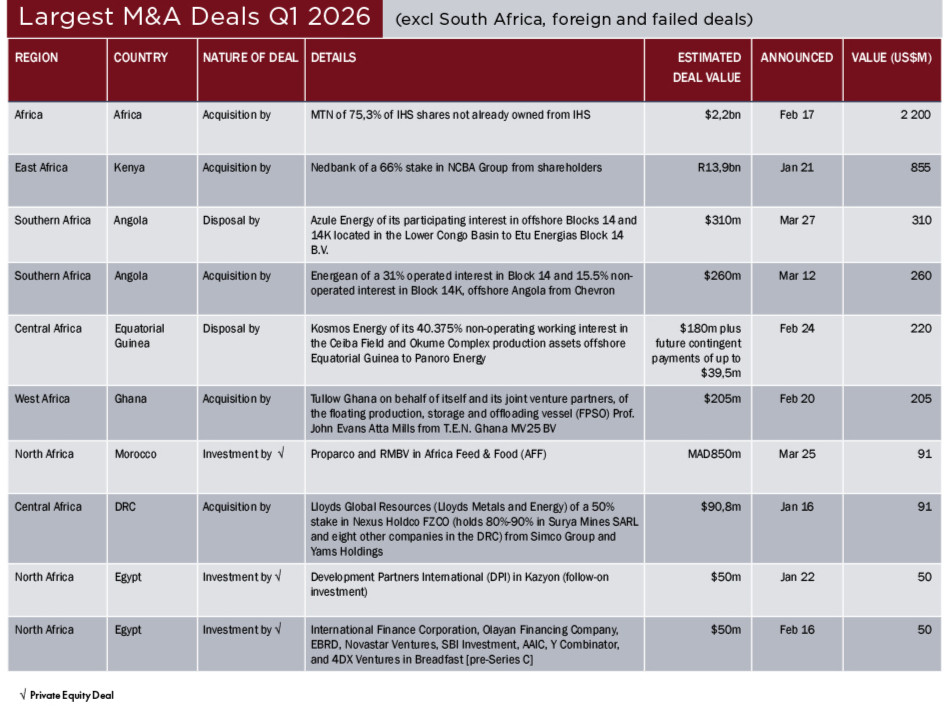

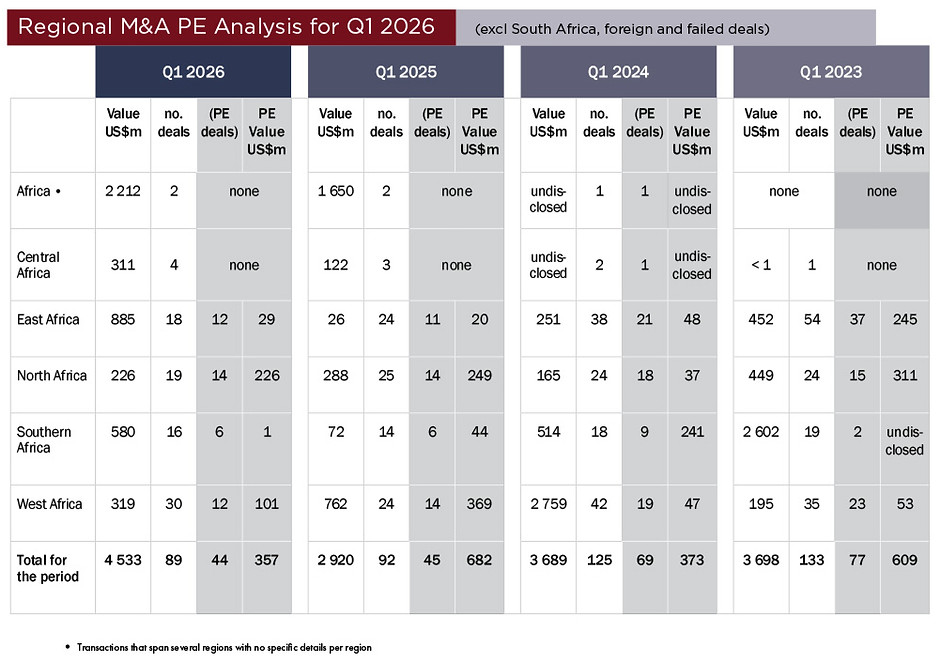

Africa’s M&A market entered 2026 with strong momentum in deal value, even as overall transaction volumes softened. In the three months to March 2026, announced deals across the continent (excluding South Africa and failed deals) reached an aggregate value of US$4,53 billion from 89 deals, compared with 92 deals valued at $2,92 billion over the corresponding period in 2025. Private equity continued to play a significant role, accounting for half of all transactions recorded during the quarter (pg 4).

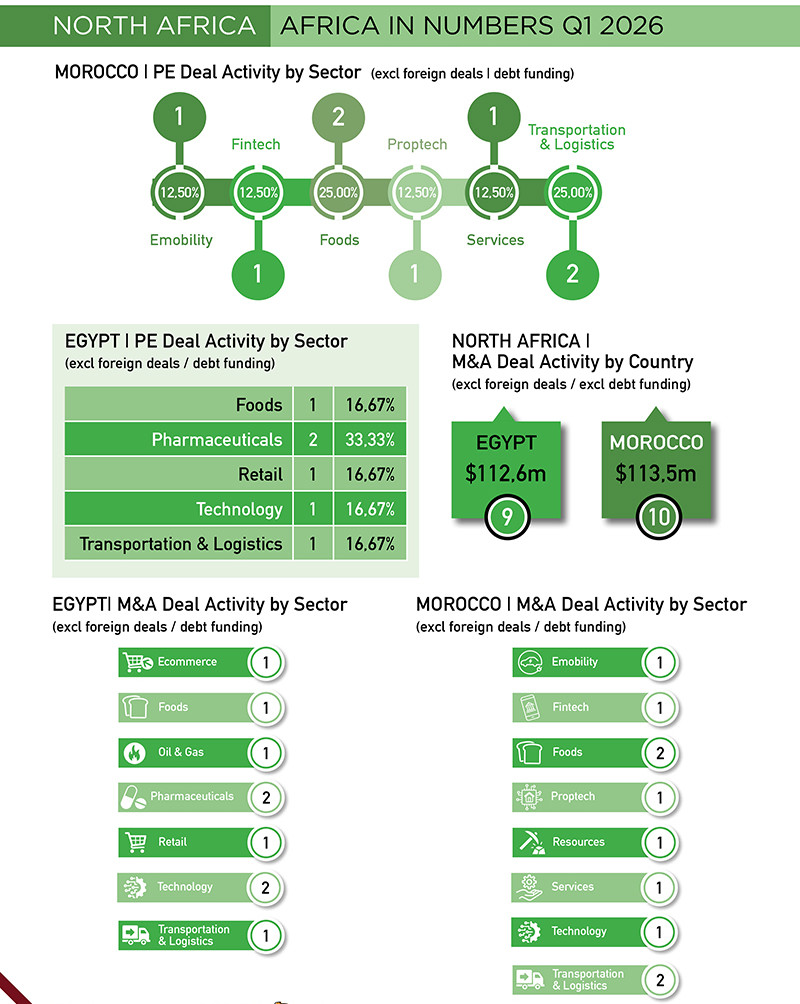

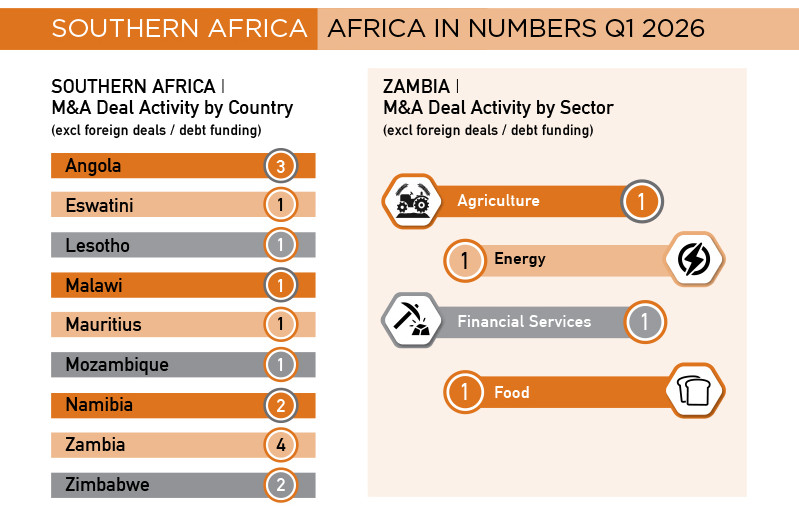

At a regional level, West Africa was, by far, the most active market, accounting for 30 deals,

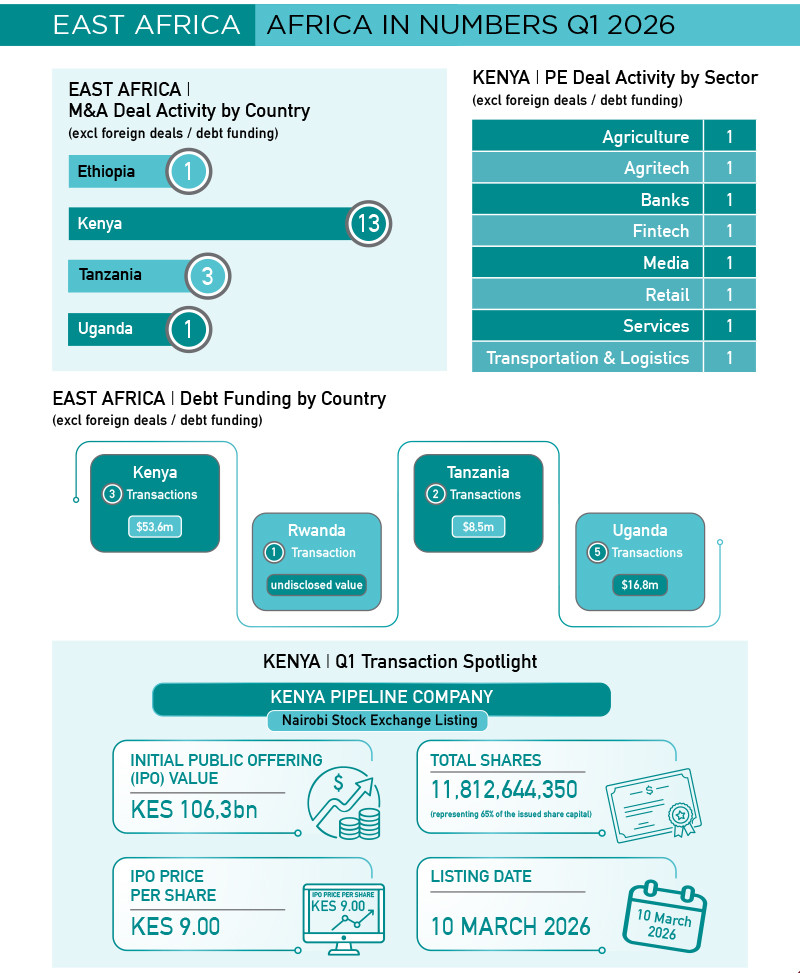

or 34% of total reported activity during the period. North Africa followed with 19 deals, and East Africa with 18. Within these regions, Nigeria (22 deals), Morocco (10 deals) and Kenya (13 deals) emerged as the key drivers of activity (pg 3).

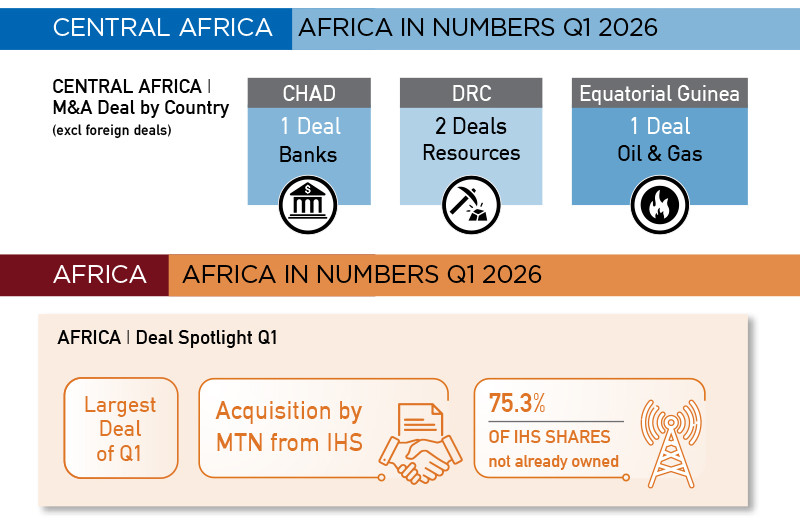

Energy and fintech remained the sectors of choice for investors across the continent. Of the top 10 deals by value announced during the quarter, four were energy transactions – two deals in Angola and one each in Equatorial Guinea and Ghana – with a combined value of $995 million. Topping the table was MTN’s acquisition of the remaining 75.3% shareholding in IHS, valued at $2,2 billion, followed by Nedbank’s acquisition of a 66% stake in NCBA, valued at $855 million (pg 6).

According to Africa: The Big Deal, Africa’s start-up funding ecosystem continues to show resilience. In the 12 months to March 2026, African start-ups raised $3,3 billion (excluding exits), comprising $1,8 billion in equity funding and $1,4 billion in debt funding. However, a closer look at the data points to an evolving funding landscape, where overall growth has increasingly been driven by a surge in debt funding, offsetting a decline in equity capital raised.

While debt and equity investors each play distinct, but equally important roles in the development of a maturing start-up ecosystem, concerns remain around the decline in smaller early-stage equity deals. According to the publication, these transactions are critical for building the next generation of companies capable of attracting larger funding rounds in future. The slowdown in early-stage activity may not immediately affect aggregate funding totals – particularly while larger equity rounds and debt transactions continue to come through – but its longer-term implications for the pipeline of scalable African businesses are worth watching.

In this issue, we feature a collection of photographs from our recent DealMakers AFRICA Annual Awards events held in Nairobi and Lagos. The March events provided an opportunity for industry participants to connect, reflect on the year past, and celebrate the achievements of 2025. Congratulations to all the winners, and thank you to everyone who joined us for the celebrations. Further details on the events, together with write-ups of the regional winners, can be found at www.dealmakersafrica.com.

Marylou Greig

DealMakers AFRICA | East Africa Awards | March 2026

DealMakers AFRICA | West Africa Awards | March 2026

THORTS

Rethinking Africa portfolios: How multinationals can navigate divestments

Daniel Outré

Too many multinational exits in Africa fail – not because of weak demand, but because the process is not adapted to the buyer universe.

Drawing on our experience as M&A advisors, we share practical reflections on what it takes to execute successful multinational exits from Africa, with a particular focus on how to manage the specificities of such processes in an African context.

A QUIET BUT STRUCTURAL SHIFT IN AFRICA’S CORPORATE LANDSCAPE

Daniel Outré

Not long ago, Unilever was, by far, the leading distribution player in French-speaking West Africa, with large fleets of trucks serving small shopkeepers across the region. The group operated asset-heavy, vertically integrated businesses, combining manufacturing facilities with extensive palm plantations for edible oil and soap production. Two decades later, most of these assets have been divested to local players, following a series of headquarters-driven decisions, culminating in a near-complete exit from the region by 2026. Unilever is now largely absent from West Africa, including key markets such as Ghana and Nigeria, where subsidiaries have either been sold or wound down. Across these markets, the group has shifted from a dominant mass-market player – with 20% to 50% market shares, strong local brands and deep operational presence – to a lighter, more selective model focused on distributing a limited range of international brands targeting higher-income consumers.

The Unilever story is just one illustration of a broader structural trend, and this evolution is neither isolated nor cyclical. Similar dynamics can be observed across sectors. While the underlying drivers may differ – including capital allocation, regulatory complexity, foreign exchange constraints and compliance considerations – the overall direction is consistent. In banking, European institutions that once held significant market shares across North and West Africa have substantially reduced their presence following the disposal of subsidiaries by Société Générale, BNP Paribas and Crédit Agricole. In the manufacturing space, groups such as Air Liquide have divested multiple African operations – including the sale of 13 subsidiaries in 2024 – as part of broader portfolio rationalisation efforts. Comparable trends are visible in other sectors, including insurance, energy and cement, where several European players have scaled back or exited their positions.

Against this backdrop, divesting multinational assets in Africa has become both more frequent and more complex, requiring processes that are carefully structured and actively managed to succeed. The remainder of this note focuses on how such processes can be adapted to local market dynamics, based on our experience advising on these transactions.

TAKING STOCK OF THE ACTUAL BUYER UNIVERSE FOR MULTINATIONALS IN AFRICA

A key starting point is that multinational assets in Africa are generally attractive and marketable, and can generate meaningful investor interest. The challenge is not the absence of demand – it is the structure of that demand. Yet many processes are delayed or weakened by recurring pitfalls, despite strong in-house M&A capabilities on the seller side. These transactions, therefore, require a specific approach, taking into account their African context.

A defining feature of the private sector in many sub-Saharan African countries is the relative lack of M&A market liquidity. A large portion of potential buyers are family-backed groups of limited to mid-scale size, and with varying degrees of sophistication and formalisation. Private equity funds and more structured regional players are also active, but few are structured to take controlling stakes, and even fewer are equipped to manage complex carve-out situations. In practice, this means that local family groups often constitute the most credible buyer universe for multinational divestments, requiring adjustments to both the positioning of the asset and the execution process. Local family groups tend to place significant value on the reputation, compliance standards and operational rigor associated with multinational assets. These assets often include long-established operations with valuable real estate, strong legacy brands and underexploited potential. Larger family groups with exposure to adjacent sectors are typically those best positioned to generate synergies and to submit the most compelling offers, particularly where assets require repositioning.

In Africa, the question is not whether there are buyers – it is whether the process is designed for them.

To address this reality, M&A advisors need to deploy a tailored toolbox. Their role is not limited to running a process, but also to designing a transaction perimeter that the market can effectively absorb. Multinational assets are often sizeable, relative to the financial capacity of local buyers, which may require restructuring the perimeter – through partial disposals, leverage optimisation or asset separation – to enhance affordability. This is particularly relevant for transactions with a significant real estate component, valuable intellectual property or a multi-country footprint, where a piecemeal approach may unlock greater value. While this increases execution complexity for the seller, it can significantly broaden the buyer universe and improve outcomes. Equally important, the gap in working cultures, transaction experience and M&A language between buyers and sellers can lead to misunderstandings and mistrust, which can, in turn, result in misinterpretations on both sides (e.g. information requests perceived as hesitation, or process discipline perceived as mistrust). In this context, the role of the advisor extends beyond execution to include active facilitation and, at times, buyer education. This is particularly true for technical aspects, such as Transition Services Agreements (TSAs), which are often critical in carve-out situations but may be unfamiliar to certain buyer profiles.

NAVIGATING THROUGH OTHER LOCAL PARAMETERS

Equally important, the seller must be fully aligned internally – across local management, regional teams and headquarters – on key parameters such as perimeter, valuation expectations, approval processes and fallback options. Misalignment at this level can quickly undermine execution. Other recurring aspects include the difficulty of transferring and repatriating funds, particularly for locally based buyers, with direct implications on transaction structuring, conditions precedent, escrow arrangements and timing. Regulatory frameworks may also lack clarity, increasing legal uncertainty around approvals and closing mechanics. These constraints can result in protracted timelines, with processes sometimes extending up to two years end-to-end – often twice as long as comparable transactions in more developed markets. Finally, confidentiality is also often an issue, as it is more difficult to preserve in an African context, with information leakages occurring more frequently. This is particularly sensitive for multinational sellers, who may be exposed to political interference or operate listed subsidiaries, increasing the potential impact of premature disclosures. In this context, communication planning should be treated as a core transaction workstream, rather than an afterthought.

Overall, Africa remains a distinct and sometimes challenging M&A environment for multinational companies. The key takeaway, however, is that the success of a divestment is rarely driven by the intrinsic quality of the asset alone, but by the ability to anticipate local constraints and structure the process accordingly.

The difference between a failed process and a successful exit is not the asset; it is the quality of the preparation.

Outré is a Partner | Enexus

THORTS

Africa’s fintech consolidation wave continues amid challenges

Konrad Fleischhauer and Kayla Jackson

After years of fragmented growth, Africa’s fintech sector has entered an era of increased consolidation, with the continent’s tech ecosystem having recorded 67 reported M&A transactions in 2025, a 72% surge from 2024, and comfortably surpassing the previous record of 40 deals set in 2022. (1) Fintech led the charge, accounting for 31 of those deals — roughly 46% of the total — as cash-rich platforms moved decisively to acquire market share, banking licences and infrastructure, rather than waiting on organic growth.

The shift is structural, not cyclical. The “growth at all costs” model that defined African tech’s venture-fuelled boom has given way to a harder-nosed calculus: profitability, regulatory moats, and scale. With African startups raising US$3,42 billion in 2025 — a healthy rebound from $2,24 billion in 2024, but concentrated in fewer hands — well-capitalised incumbents are well positioned. Increased partnerships and expansions also complemented M&A, as firms like Nigeria’s Rank (ex-Moni) snapped up AjoMoney and Zazzau Microfinance Bank for savings and credit services, and South African payments specialist, Stitch Group (2) similarly acquired ExiPay and Efficacy Payments to bolster its infrastructure.

THE DEALS DRIVING THE NARRATIVE

Two transactions encapsulate the moment. In Nigeria, Moniepoint completed its acquisition of a 78% stake in Kenya’s Sumac Microfinance Bank. Sumac, a licensed deposit-taking lender, gives Moniepoint instant access to Kenya’s $67,3 billion mobile payments market, bypassing a lengthy regulatory process. After an earlier attempt to acquire payments firm KopoKopo fell apart, Moniepoint pivoted to Sumac and secured this East African foothold (retaining Sumac’s infrastructure and staff),(3) (4) while also grabbing UK’s Bancom Europe for broader capabilities.(5)

Konrad Fleischhauer

Kayla Jackson

In South Africa, Lesaka Technologies sealed a transformative $61 million (R1,1 billion) deal for Bank Zero in 2025. (6) Bank Zero brought more than R400 million ($22 million) in deposits and over 40,000 funded accounts to the transaction, embedding a zero-fee neobank into Lesaka’s platform for consumers, merchants and enterprises. Chairman Michael Jordaan, the former FNB CEO who co-founded Bank Zero, joined Lesaka’s board post-deal, signalling governance depth. (7)

Both deals follow the same playbook: acquire a licence, retain the team, accelerate the model.

VC-TO-PE SHIFT FUELS EXIT STRATEGIES

The M&A wave is inseparable from a broader shift in how capital flows in and out of African tech. With global IPO markets subdued, the traditional venture-to-public-markets exit path has narrowed, and Private equity (PE) is filling the gap. The African Private Equity and Venture Capital Association (AVCA) noted 63 exits in 2024 – up 50% year-on-year – with secondary transactions now accounting for a third of all exits. PE suits the new African tech reality: predictable recurring revenues in payments application programming interfaces, software as a service infrastructure, and lending platforms translate more cleanly into PE return models than into volatile public market multiples.

GEOGRAPHY, REGULATION, AND THE ROAD AHEAD

Three-quarters of Africa’s 2025 tech M&A activity was concentrated in Africa’s “Big Four” markets — South Africa (16 deals), Kenya (14), Egypt (11) and Nigeria (9) — the same markets that attracted the lion’s share of 2025 funding: $933 million, $811 million, $548 million, and $438 million respectively. The correlation is not coincidental. More mature ecosystems attract capital, which breeds acquirers, which deepens ecosystems further. The flywheel is turning.

The regulatory dimension is equally important. Across the continent, buying a licensed institution compresses years of compliance into a single transaction, as illustrated by Moniepoint’s Sumac play. In markets where regulatory frameworks are tightening, licence acquisition will continue to gain strategic importance.

Looking to the remainder of 2026, it is likely that the above trends will continue, although the current global economic uncertainty may have an impact – not least on the continued appetite of Gulf sovereign wealth funds for African fintech assets – while regulatory delays, valuation gaps between founders and buyers, and currency volatility will remain challenges. That said, the direction of travel is clear, with consolidation in Africa’s fintech sector set to continue.

Fleischhauer and Jackson are Corporate Financiers | PSG Capital

-

Efficacy Payments has been acquired by Stitch Group, enabling the Group to offer card acquiring services

-

https://techcabal.com/2025/06/02/moniepoint-kenya-sumac-78-kopokopo/